It’s early, but a hurricane could threaten the Gulf Coast not this weekend but next.

We are just past the peak of hurricane season, and a potential storm in the Gulf of Mexico has caught the attention of weather models. While it is still a week out, and predictions could change, now is the time for insurers, policyholders, and legal professionals to start paying attention. Whether managing insurance risks, protecting your home or business, or handling hurricane-related claims, premature action based on these models can help you be better prepared.

Early Hurricane Forecast Models: AI (Artificial Intelligence) vs. GFS (Global Forecast System)

Weather forecasting has improved tremendously, and two key models—the AI-based European model and the GFS (Global Forecast System)—show a storm could potentially affect the Gulf Coast one week from now. However, these models differ in the storm’s potential strength and exact path. Here is what the current data shows and why it matters.

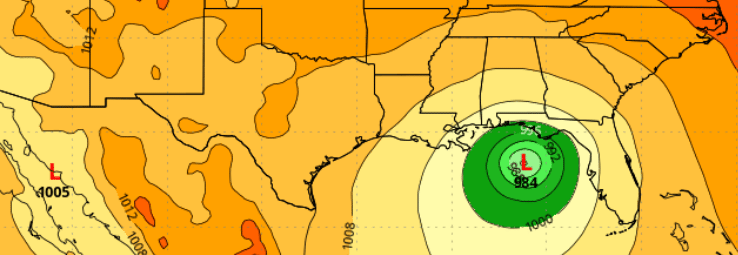

AI Weather Model (Image 1)

1. Storm Overview:

The AI model shows a strong storm brewing in the Gulf of Mexico, with a central pressure of 984 hPa (hectopascals). This indicates an intense storm, as lower pressure means stronger winds and more intense storms. The model suggests landfall near the panhandle of Florida, with winds and rain spreading outward. For insurers and policyholders, communicating now would be a good idea. Again I want to stress this is VERY early and things can change.

2. Possible Impacts:

If this model is accurate, insurers and policyholders along the Gulf Coast should brace for intense winds and significant flooding risks. Those in the energy sector should also prepare for potential disruptions to oil rigs and refineries, which can affect business continuity. Legal professionals might start considering the types of claims that could arise, such as flood and wind damage claims, especially around homes and businesses with high value coverage. Of course, as always, safety comes first, and listening to local officials is the most important currently.

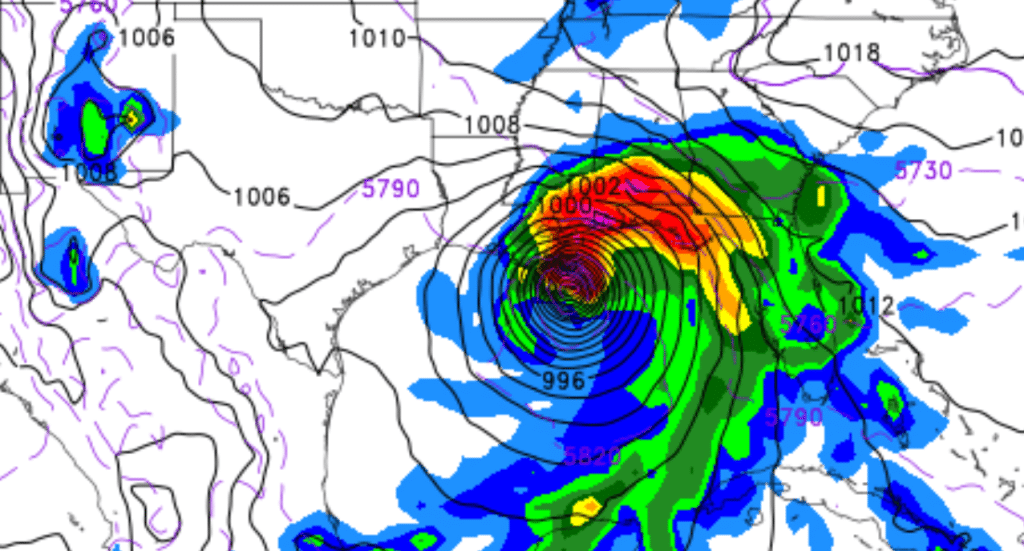

GFS Weather Model (Image 2)

1. Storm Overview:

The GFS model shows a similar storm forming in the Gulf but with a central pressure of 996 hPa—still indicating a potent storm. Pressure is a good weather element that shows how strong a storm can be. The predicted path appears slightly further West, with landfall closer to Mississippi or Alabama. Again, it is too early to know precisely what will occur, but it is time to start thinking about it.

2. Strength and Structure:

The GFS model indicates a wide storm, potentially spreading over a larger area but still with intense winds and rainfall. A storm like this could still cause widespread flooding and power outages.

3. Possible Impacts:

Insurers should be aware of the potential large area affected, which could lead to many claims, as we know. Policyholders along the Gulf Coast should ensure their hurricane deductibles are ready, and business owners should review their insurance for flood and windstorm coverage. Lawyers may want to begin reviewing potential business interruption claims, particularly for those outside the direct path but still affected by a power loss or storm surge.

Why This Matters to Insurers, Policyholders, and Lawyers

For Insurers:

Risk Management: Understanding early storm forecasts helps insurers assess potential claims and prepare for the volume of policyholders likely to be impacted.

Underwriting and Communication: This is the time to contact policyholders, ensure they understand their coverage, and, where necessary, make policy adjustments. Communication around flood insurance and hurricane deductibles should be a priority.

For Policyholders:

Check Your Coverage: Now is the time to review your insurance policies. Many homeowners are unaware that standard homeowners’ policies do not cover flood damage. This is especially important given the flooding risks both models suggest. If you are a business owner, check your business interruption coverage.

Prepare for the Storm: While the models provide early information, it is essential to use this time to secure your property. Everyone should take steps to back up important documents, have storm shutters ready to go, and clear any debris that could become hazardous, regardless of the storm’s exact path.

For Lawyers:

Anticipate Claims: Hurricane season often leads to an influx of claims involving property damage, business interruption, and personal injury. Early forecasts allow legal professionals to prepare for client inquiries about coverage, especially where disputes over policy terms and storm damage liability may arise.

Business Continuity and Liability: Attorneys handling corporate clients, especially those in coastal regions, should start reviewing contracts related to hurricane preparedness and response. Businesses may face liability if they are not adequately prepared, and legal advice could be sought early.

It is still early and so much can change.

Remembering that hurricane forecasting models are imperfect, mainly when predicting storms more than five days in advance, is essential. As new data is added to these models, a lot can change—both in the storm’s path and intensity. The AI model could be too far East, but the GFS model may be closer to the actual outcome, or vice versa. The key takeaway here is preparedness. While the exact outcome is uncertain, now is the time to take precautions and prepare for what is to come.

Hurricanes can be unpredictable, but early warning models like the AI and GFS gives us the opportunity to take necessary precautions. Whether you are an insurer calculating risk, a policyholder reviewing your coverage, or a lawyer preparing for potential storm-related cases, staying informed, and acting early can make all the difference. Keep checking for updates as the models evolve, and remember, preparedness today can save you from significant headaches.

– Insurers: Reach out to policyholders to review their coverage and suggest any necessary updates.

-Policyholders: Check to make sure your insurance is current and that you have adequate coverage for flooding, wind damage, and other hurricane-related risks.

– Lawyers: Begin reviewing client contracts and preparing for potential legal inquiries related to hurricane preparedness and storm damage claims.

You know I will keep you updated.